and the distribution of digital products.

China goes big on stimulus to recover from stagnation

Today, enjoy the On the Margin newsletter on Blockworks.co. Tomorrow, get the news delivered directly to your inbox. Subscribe to the On the Margin newsletter.

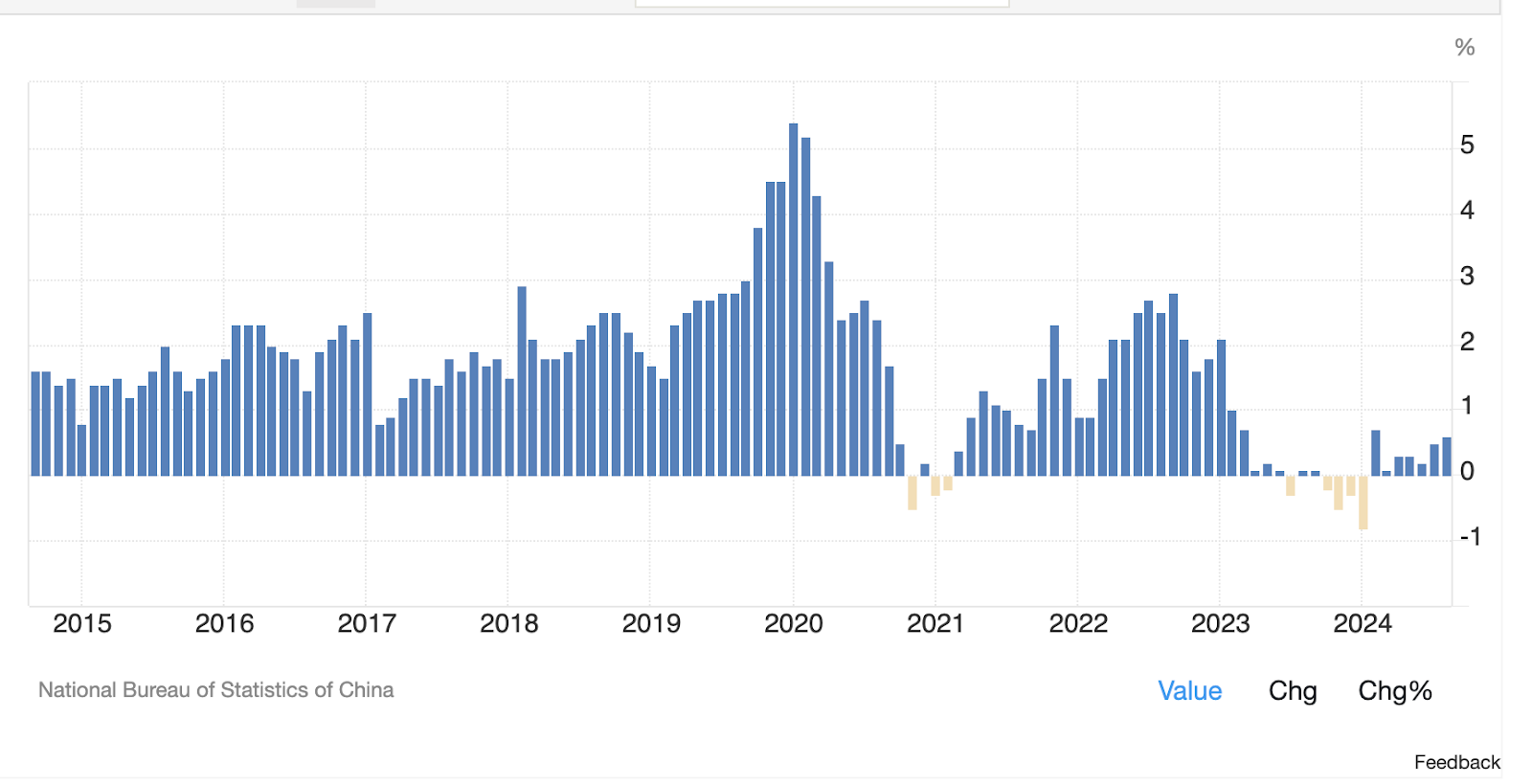

China never really recovered from the COVID pandemic like the US has, and has been stagnating and bleeding ever since.

For what was previously the global powerhouse of economic growth, we can see that China’s inflation has been flat at best, and outright deflationary at worst:

There are a few reasons why the nation has been so stagnant. The primary one is that China is in the early stages of a balance sheet recession (as explained in a recent Forward Guidance episode).

A balance sheet recession, as coined by Richard Koo, occurs when high levels of private sector debt causes businesses and households to focus on repaying that debt rather than spending or investing. This in turn leads to economic stagnation. This recession type is characterized by a need to repair balance sheets, where conventional monetary policies like lowering interest rates may be less effective, and fiscal policy might be more crucial for recovery.

The balance sheet recession that China has been experiencing has recently begun to accelerate, leading many to believe that China is going to miss its intended annual goal of 5% GDP growth. This led to Chinese bond yields absolutely cratering in a flight to safety trade as Chinese equities bled constantly:

However, ever since the US Fed announced its first rate cut and the cutting cycle began, the Chinese government has taken this as the green light to go big on stimulus. Due to both governments easing in tandem, China can do so without as much currency rate risk.

In quick succession, the Chinese government has announced new monetary and fiscal policies.

Monetary policies:

- Reserve requirement ratio (RRR) cut: reduced by 50-basis points to boost lending activities.

- Mortgage rate cut: cutting interest rates for existing mortgages and lowering minimum down payments to 15% on all types of homes.

- Launch of new monetary policy tools: PBOC Governor Pan Gongsheng announced new lending facilities aimed at providing buying pressure on Chinese equities.

Fiscal policies:

- Sovereign debt issuance: plan to issue $284 billion in sovereign debt as part of the fiscal stimulus.

- Fiscal spending order: President Xi ordered sufficient fiscal spending, with details expected in October.

- China will distribute a one-time allowance to disadvantaged people ahead of a national holiday next week, a government statement said.

It’s clear that China is committed to throwing everything they can at the wall until something sticks and things improve. Luckily, with all other global central banks in an easing bias (apart from Japan), China has the currency cover to do so.

The big question at hand now is: Will it be enough for China to recover? We simply don’t know. However, FXI (iShares China large-cap ETF) is up 16% over the past five days, and setting some of the largest daily gains in history is surely a positive sign that Chinese authorities are getting underneath this thing.

— Felix Jauvin

$184.4 millionThe amount of inflows BlackRock’s spot bitcoin ETF posted on Tuesday, according to data from Farside Investors. The figure breaks the September record for daily inflows to a single fund.

IBIT’s inflows come amid a broader streak for spot bitcoin ETFs in the US. The 11 products collectively have posted inflows for the past five trading days.

What Wall Street expects from the August PCE reportThe Fed’s preferred inflation gauge (PCE) is slated to drop tomorrow morning.

Here’s a quick review of what analysts are expecting and how we’d interpret different outcomes:

Headline PCE is predicted to come in at 2.3% higher year-over-year in August. This would represent a decline from the 2.5% figure reported in July and would also put annual inflation at its lowest point in four years.

Analysts expect core PCE (excluding volatile food and energy prices) to increase slightly and come in 2.7% higher annually, as compared to 2.6% in July.

Preston Caldwell, senior US economist at Morningstar, is forecasting a 0.15% increase in overall PCE. He says core PCE will come in at 1.9% annualized over the past three months and at 2.4% over the past six months.

Should his predictions come true, Caldwell believes this will set up the FOMC for two additional 25bps rate cuts, one in November and one in December.

Remember, the latest dot plot shows that most committee members see us ending 2024 50bps lower than where we currently stand. Fed fund futures markets on Thursday put the odds of a 50bps cut in November at 53%.

The report will be published at 8:30 am ET Friday. Stay tuned for our recap in On the Margin.

— Casey Wagner

Harris, Democrats quietly court crypto industryVice President Harris continues to cautiously signal to crypto-focused voters that she intends to be more supportive of the industry than the current administration is.

In a speech Tuesday evening at the Economic Club of Pittsburg, Harris promised that under her leadership, the US will “remain dominant in AI, quantum computing, blockchain and other emerging technologies.”

The comments coincide with an apparent broader push in the Democratic Party to change the narrative around crypto. Sen. Elizabeth Warren, arguably one of the industry’s biggest adversaries on the Hill, told Semafor she “has no problem with people buying and selling crypto.”

“We need to make sure we have curbs in place, like we do in every other part of our financial system, so that crypto can’t be used by terrorists, drug traffickers and rogue nations,” she added. Now that sounds more like the Warren we know.

Still, the shift from Dems — slight as it may be — is significant.

To be clear, I am not saying that Harris is going to be a pro-crypto president (I haven’t said that about Trump, either). Trump’s efforts to woo the industry have, in my opinion, forced the Harris camp to address the topic, and now we have both candidates talking about digital assets.

That’s just not a reality I had foreseen even one year ago.

Maybe now we’ll see an actual, formal crypto platform from either one of them, although I wouldn’t hold my breath.

— Casey Wagner

Bulletin Board- Worldcoin’s native WLD token is surging following recent reports that OpenAI is looking to shift to a for-profit model. Sam Altman, OpenAI’s CEO, is also the co-founder of Worldcoin, a cryptocurrency project focused on using biometrics to confirm identity. WLD is up 4% over the past 24 hours and more than 30% in the past week.

- New York City Mayor Eric Adams faces five federal public corruption charges, a newly unsealed indictment reveals. Adams had previously been viewed by many as a pro-crypto politician, promising in 2022 that he would take his first three paychecks as mayor in cryptocurrency, a plan that was ultimately thwarted by the US Department of Labor.

- SEC Chair Gary Gensler and billionaire investor Mark Cuban posed for a photo on the set of CNBC’s Squawk Box. Whether the pic was snapped before or after Cuban told the world he’d like to take Gensler’s job remains unknown.

Start your day with top crypto insights from David Canellis and Katherine Ross. Subscribe to the Empire newsletter.

Explore the growing intersection between crypto, macroeconomics, policy and finance with Ben Strack, Casey Wagner and Felix Jauvin. Subscribe to the Forward Guidance newsletter.

Get alpha directly in your inbox with the 0xResearch newsletter — market highlights, charts, degen trade ideas, governance updates, and more.

The Lightspeed newsletter is all things Solana, in your inbox, every day. Subscribe to daily Solana news from Jack Kubinec and Jeff Albus.